Privately pooled investment funds in India have traditionally operated through structures such as trusts, companies and limited liability partnerships. While each of these vehicles can accommodate investment activity, none was originally designed specifically for the operational requirements of a fund structure. A company, for instance, operates within a fixed-capital framework, where returning capital to investors generally requires compliance with formal processes such as a court-approved reduction of capital or a permitted buy-back

Similarly, existing structures do not provide statutory segregation of multiple investment strategies within a single vehicle. Where different schemes or strategies are housed together, the protection between such pools is generally dependent on contractual arrangements rather than a dedicated statutory mechanism. This limitation becomes particularly relevant when Indian fund managers seek to attract overseas investors, as global investors are more familiar with corporate fund vehicles that permit flexible capital movement and are recognised across major financial jurisdictions.

The Variable Capital Company (VCC) model seeks to address this structural gap by providing a purpose-built corporate framework for pooled investment activities.

I. What is a Variable Capital Company?

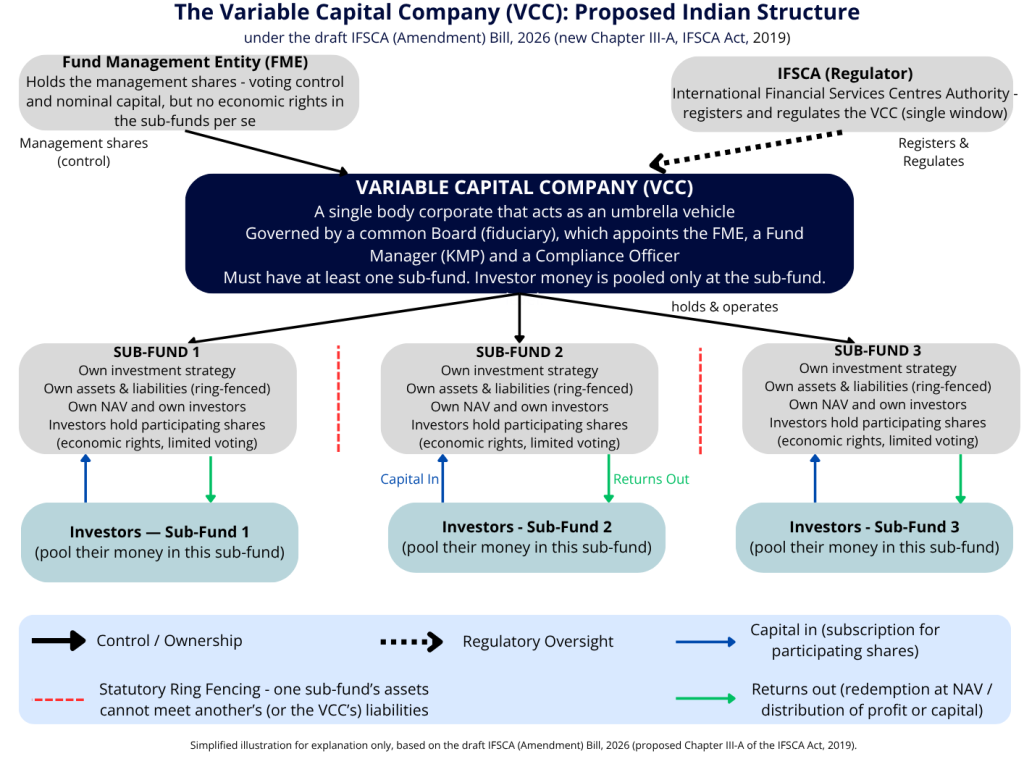

A Variable Capital Company, or VCC, is a body corporate designed to hold investments on behalf of a group of investors. The structure allows multiple investment strategies, each distinct from the other, to operate within the same corporate framework. It generally follows a two-tier model comprising an umbrella entity at the top and one or more “sub-funds” below it, with the respective sub-funds undertaking the investment activities.

This arrangement enables fund managers to aggregate investments from multiple investors while maintaining separate investment strategies within a single overarching structure.

The defining feature of a VCC is reflected in the term “variable”. Unlike a conventional company where share capital is comparatively fixed and changes to capital require prescribed corporate law procedures, a VCC is structured to permit greater flexibility in managing capital. It may issue shares when investors contribute funds and facilitate redemption or buy-back of shares when investors exit, without requiring the same procedural framework applicable to ordinary companies.

Such flexibility is particularly significant for investment funds, where investors may enter and exit at different stages and expect their interests to be valued with reference to the prevailing Net Asset Value (NAV).

II. The VCC in India

India does not yet have a VCC law in force. What exists is a proposal, shaped by two expert committees and a draft amendment bill.

The first committee, chaired by Dr. K. P. Krishnan, reported in May 2021. It studied VCC-type structures in other countries and recommended that India allow a similar structure in its International Financial Services Centre (IFSC) at GIFT City.[1]

The second committee, chaired by Dr. M. S. Sahoo, reported in October 2022. It prepared the legal framework and recommended placing the VCC inside the existing IFSCA Act, so that a single law and a single regulator would govern it.[2] In preparing this framework, Dr. Sahoo’s report opened an economic gateway for funds and paved the path for the Indian fund industry to compete at the global level.

This led to the draft International Financial Services Centres Authority (Amendment) Bill, 2026, (“Draft Bill”) which proposes to insert a new Chapter III-A into the IFSCA Act, 2019. The proposed chapter seeks to create a dedicated statutory framework for VCCs in IFSC, thereby providing legal recognition, regulatory certainty, and operational clarity for their establishment and governance. At the time of writing of this piece, it is a consultation draft and has not yet been passed by Parliament.[3]

The proposed VCC framework for the IFSC is best read as an adaptation, not a copy. The committees studied foreign models but designed the structure to fit India’s regulatory setup. For example, under the proposed framework a VCC must always have at least one sub-fund; a requirement embedded in the VCC’s articles (its constitutional document), so that, by its very constitution, it is meant to work as an umbrella for pooled schemes rather than as a stand-alone company.[4]

III. The VCC in Other Countries

The VCC idea is not new. Several countries already use company structures with variable capital for funds.

Singapore is the best-known recent example. Its Variable Capital Companies Act came into force in 2020 and was adopted quickly. India’s proposal draws most heavily on the Singapore model.[5]

Luxembourg has long used a similar vehicle called the SICAV (Société d’Investissement à Capital Variable), an investment company with variable capital that can run many ring-fenced compartments within one entity.[6] Mauritius also passed its own Variable Capital Companies Act in 2022.[7] The Cayman Islands achieves a similar effect through the segregated portfolio company.[8]

The common thread among all these structures is simple: large investors prefer structures they already understand, and a country that offers such a structure finds it easier to attract fund business.

IV. How a VCC Works?

Under the Draft Bill, a VCC works on two levels. At the top sits the VCC itself, as an umbrella company. Beneath it sit one or more sub-funds. Each sub-fund is a distinct pool of money with its own investment strategy, its own investors and its own accounts. The pooling of money happens at the sub-fund level, not at the VCC level.[9]

Capital comes into a VCC in three forms. The first is management shares. These are usually held by the fund management entity (FME) and they carry voting control over how the VCC is run and structured, for example appointing the Board. They also represent the VCC’s nominal set-up capital. Management shares carry no economic rights in the sub-funds per se; the FME is instead paid for its work through management fees. However, in order to maintain its statutory continuing interest in a sub-fund it has to subscribe to participating shares as well, in which case it holds economic rights in that sub-fund like any other investor.

Participating shares are the investors shares, issued at the sub-fund level; they carry the economic rights; the right to that sub-fund’s gains and only limited voting rights with respect to the variation of an existing right of an investor. A VCC may also issue redeemable debentures, which carry no vote.[10] The VCC is run by a single Board, which owes fiduciary duties and appoints an IFSCA-registered FME, a fund manager (treated as key managerial personnel) and a compliance officer. The FME and the fund manager manage the investments of all the sub-funds, while the compliance officer is responsible, at the VCC level, for the VCC’s legal and regulatory compliance.[11]

A key feature is ring-fencing. The assets and liabilities of each sub-fund are kept legally separate from every other sub-fund and from the VCC itself. If one sub-fund runs into trouble, its losses stay within it and cannot be used to pay another sub-fund’s debts. This protection comes from the statute, not merely from contracts unlike other existing fund structures in India. Further, a sub-fund cannot sue or be sued in its own name; any claim relating to a sub-fund is brought by, or against, the VCC, which acts on the sub-fund’s behalf. The Draft Bill does, however, allow the VCC to set off claims between its sub-funds as if each were a separate legal person – a limited legal fiction.[12]

The VCC’s accounts follow the same separation. Under the Draft Bill, no asset, no liability, no income or expenditure is held to VCC’s own account; items attributable to a sub-fund are allocated to that sub-fund, and items not attributable to any single sub-fund are apportioned across the sub-funds on a fair basis.[13] Each sub-fund accordingly carries its own assets, liabilities, income and net asset value.

The Draft Bill separately requires the VCC to prepare, for itself and for each of its sub-funds, books of account and financial statements, including consolidated financial statements, in accordance with the applicable accounting standards. The Board must also prepare a report giving a true and fair view of the operations of the VCC and its sub-funds. These statements and the Board’s report are to be provided to the IFSCA in the manner and within the time specified by regulations.[14]

Investors enter and exit by buying and redeeming shares at NAV and as capital is variable, the sub-fund can issue, redeem and buy-back these participating shares, cancelling them on redemption or buy-back, without the procedural formalities an ordinary company faces.[15] This is the main difference from a fixed-capital company, which is built to keep its capital stable. How often this can happen depends on the fund: an open-ended sub-fund may allow investors to enter and exit on a recurring basis, whereas a closed-ended sub-fund usually allows exit only at defined points or on winding up.

V. How Are Investors Paid?

Investors in a VCC can receive money in two main ways. The first is redemption, which is essentially an exit. The investor hands its participating shares back to the sub-fund, which buys them back and cancels them at NAV, and pays the investor their current value. This may be done in full (a complete exit) or in part, partial redemption is permitted, so an investor can take some money out while staying invested for the rest.[16] The second is distribution, where the investor keeps its shares and the sub-fund pays out a sum on them, much like a dividend. A distribution can be made from two sources: out of profits (the gains the sub-fund has made), or out of capital (the pooled capital of the sub-fund together with the accretions to it, which include profits of earlier years that have been capitalised from reserves). This is where a VCC differs from a normal company. Under the Companies Act, 2013, a company can generally pay dividends only out of profits (section 123), and the principle of capital maintenance restricts the return of capital employed to shareholders; reducing a company’s share capital requires a special resolution and the approval of the National Company Law Tribunal under section 66, because that capital is meant to stay in the company to protect its creditors.

A sub-fund of a VCC is not bound in the same way: it can make a distribution out of capital as well, not only out of profits. This lets the sub-fund pay investors out of the actual cash it receives rather than wait for accounting profit, so the manager can return money as cash comes in, for example as investments are partly sold even in a year when the fund’s investments have not been fully realized or their value has dipped for the time being. It also lets the manager return surplus cash that cannot yet be deployed instead of leaving it idle, which helps preserve both returns and the manager’s track record. This is also what distinguishes a distribution out of capital from a redemption: in a redemption the investor gives up its shares and exits, whereas in a distribution out of capital the investor keeps all its shares and simply receives a payment drawn from the sub-fund’s capital pool.

VI. VCC Compared with a Trust, a Company and an LLP

In India, funds have so far been set up mainly as trusts, and sometimes as companies or limited liability partnerships (LLPs). Each form has limits when used as a fund. The table below compares them on the points that matter most for pooled investment.[17]

| Feature | Trust | Company | LLP | VCC |

| Legal nature | A fiduciary relationship between settlor, trustee and beneficiaries (investors); not a separate legal person | A separate legal person | A separate legal person | A separate legal person, built specifically for funds |

| Capital flexibility | Flexible, but contractual | Rigid by law | Flexible but cumbersome | Flexible by law |

| Ring-fencing | Segregation by contract (through trust deed) | No statutory ring-fencing | No statutory ring-fencing | Statutory ring-fencing |

| Investor rights held as | Beneficiary under the trust deed | Shareholder | Partner | Shareholder of a sub-fund (participating shareholder) |

| Suitability for funds | Widely used, but not globally aligned | Poor fit due to rigid capital & other constraints | Limited use due to statutory limits on entry & exit of investors | Specifically augmented for pooled funds as globally familiar & ability to house multiple strategies under one roof |

VCC in IFSC is still at the proposal stage. In essence, the proposed framework offers a single body corporate that holds one or more ring-fenced sub-funds, lets capital move in and out freely as investors enter and exit at NAV, and allows returns to be paid out of profit or out of capital; a combination that a trust, a company or an LLP can each achieve only in part, and largely through contract rather than by statute. If enacted, it could give Indian fund managers a purpose-built vehicle of a kind so far available mainly offshore and it raises a broader question for the future: if the structure works well in the IFSC, should a similar vehicle be considered for the Indian mainland, under SEBI, for domestic funds? As you consider it, one further question is worth keeping in mind: Should India evaluate the VCC model more closely as a fund-structuring option, particularly from the point of view of fairness, investor protection and the management of conflicts of interest?

[1] Int’l Fin. Servs. Ctrs. Auth., Report of the Expert Committee on the Feasibility of the Variable Capital Company in International Financial Services Centres in India (K. P. Krishnan, Chairperson, 26 May 2021) [hereinafter Krishnan Committee Report].

[2] Int’l Fin. Servs. Ctrs. Auth., Report of the Expert Committee for Drafting a Legal Framework for Allowing Variable Capital Company Structure in the IFSCs (M. S. Sahoo, Chairperson, 12 October 2022) [hereinafter Sahoo Committee Report], Part A, para 2, at 11.

[3] Draft Bill, supra note 1, cl. 2 (insertion of Chapter III-A into the IFSCA Act, 2019).

[4] Draft Bill, supra note 1, s. 13B(b) (an Indian VCC must have at least one sub-fund).

[5] Variable Capital Companies Act 2018 (Sing.), in force 14 January 2020.

[6] On the Luxembourg SICAV (société d’investissement à capital variable), see the Law of 10 August 1915 on commercial companies and the related Luxembourg fund laws.

[7] Variable Capital Companies Act 2022 (Act 3 of 2022) (Mauritius).

[8] Companies Act (Cayman Islands), provisions on segregated portfolio companies.

[9] Draft Bill, supra note 1, s. 13C(1) and (3) (pooling occurs at the sub-fund level; no asset or liability is held to the VCC’s own account).

[10] Draft Bill, supra note 1, ss. 13O and 13R (management shares, participating shares and redeemable debentures).

[11] Draft Bill, supra note 1, s. 13W (a variable capital company is governed by a common Board, which appoints the fund management entity, the fund manager as key managerial personnel and a compliance officer; the compliance officer is responsible for the company’s legal and regulatory compliance).

[12] Draft Bill, supra note 1, s. 13C (a sub-fund is not a legal person separate from the variable capital company; it may sue or be sued only through the company, which may exercise set-off between sub-funds as if each were a separate legal person)

[13] Draft Bill, supra note 1, s. 13C(3) (income, expenditure, assets and liabilities attributable to a sub-fund are allocated to it, and items not attributable to any single sub-fund are apportioned across the sub-funds on a fair basis).

[14] Draft Bill, supra note 1, s. 13Y (a variable capital company must, for itself and each sub-fund, maintain books of account and prepare financial statements, including consolidated financial statements; the Board must prepare a report; and these are to be furnished to the Authority in the manner and time specified by regulations).

[15] Draft Bill, supra note 1, s. 13S(3) (on buy-back or redemption of participating shares, the shares are cancelled and the issued share capital is reduced by the amount paid).

[16] Draft Bill, supra note 1, s. 13B(d) and Illustration (a variable capital company may alter participating share capital at any time, including by further issuance, conversion, buy-back and redemption; in the Illustration, an investor redeems 5,000 of 10,000 participating shares — i.e. a partial redemption — at the prevailing net asset value).

[17] Funds in India are most commonly set up as trusts under the SEBI (Alternative Investment Funds) Regulations, 2012, read with the Indian Trusts Act, 1882; companies are governed by the Companies Act, 2013 and LLPs by the Limited Liability Partnership Act, 2008.