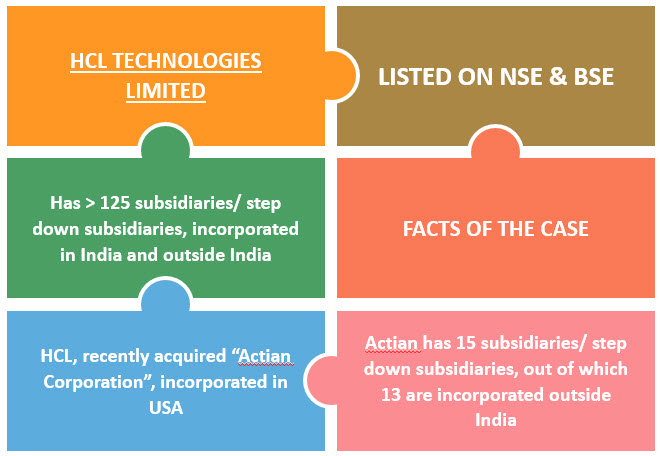

SEBI vide its interpretative letter dated May 30, 2019, in the matter of HCL Technologies Limited (“listed entity”/ “the Company”/ “HCL”), has come out with an informal guidance in connection with Regulation 46 of SEBI (Listing Obligations & disclosure Requirements) Regulations, 2015 (“Listing Regulations”).

In the said letter, the SEBI’s guidance was sought pertaining to disclosure of financial statements of foreign subsidiaries/ step down subsidiaries on the website of the listed entity in terms of Reg 46(2)(s) of Listing Regulations.

Reg 46 contains the mandatory contents which are required to be disclosed on the website of any listed entity, which inter-alia include, separate audited financial statements of each subsidiary of the listed entity in respect of a relevant financial year to be disseminated at least 21 days prior to the date of the AGM which is called inter alia to consider accounts of that financial year.

| The brief gist of the said informal guidance letter is as follows: |

|

|

| Governing Legal Provision: |

| i. | Reg 46(2)(s), as mentioned in the preceding paragraphs; and |

| ii. | Section 136(1) to Companies Act, 2013 |

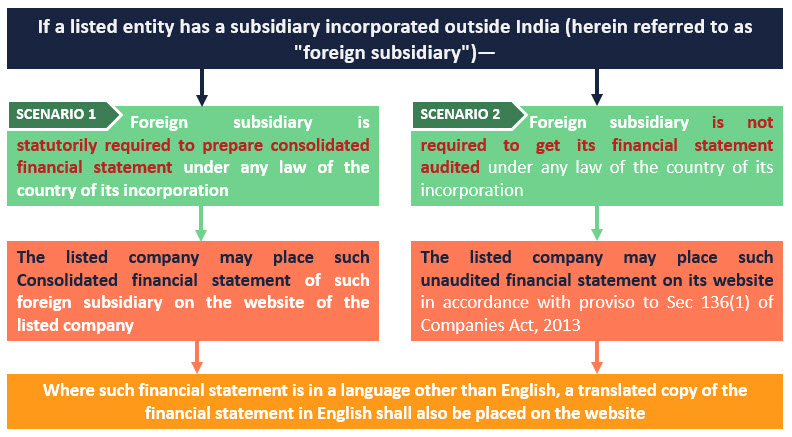

| MCA, vide its notification dated February 09, 2018, has already granted a relaxation to the listed companies having foreign subsidiaries, with regard to dissemination of the audited financials of the subsidiaries on its website respect of foreign subsidiaries whose accounts are not required to be audited in terms of the laws of the country where such subsidiaries are incorporated. |

|

The proviso to Reg 136(1) states the following: “Provided also that every listed company having a subsidiary or subsidiaries shall place separate audited accounts in respect of each of subsidiary on its website, if any: Provided also that a listed company which has a subsidiary incorporated outside India (herein referred to as “foreign subsidiary”— (a) where such foreign subsidiary is statutorily required to prepare consolidated financial statement under any law of the country of its incorporation, the requirement of this proviso shall be met if consolidated financial statement of such foreign subsidiary is placed on the website of the listed company; (b) where such foreign subsidiary is not required to get its financial statement audited under any law of the country of its incorporation and which does not get such financial statement audited, the holding Indian listed company may place such unaudited financial statement on its website and where such financial statement is in a language other than English, a translated copy of the financial statement in English shall also be placed on the website.” |

| Guidance sought: |

|

| SEBI views: |

| SEBI, in line with the Proviso to Sec 136(1) of the Companies Act, 2013, gave its views on the guidance so sought, which are as under: |

|

For further clarifications or information, you can reach us @

Anjali Aggarwal

(Partner)

+91 9971673336

anjali@indiacp.com