A closer look at how SEBI’s lock-in framework operates across Mainboard and SME IPO transactions.

Every IPO transaction carries a lock-in obligation, and, in the experience of most practitioners, it receives less analytical attention than it deserves. Lock-in is frequently approached as a disclosure exercise: a set of periods to be identified and recorded in the offer document. That approach is risky.

The lock-in analysis should begin with identifying who qualifies as a promoter of the issuer, which securities can count towards the minimum promoters’ contribution and what constitutes excess promoter holdings. If these questions are not tested in the correct sequence, the consequences may surface in the offer document, depository lock-in marking and post-listing obligations.

The framework governing lock in mechanism under the SEBI ICDR Regulations, 2018 is more layered than it first appears. For promoters, the lock-in operates through two distinct buckets carrying separate lock-in periods, rather than as a single uniform restriction on the entire promoter holding. It also differs between Mainboard and SME IPOs, with the SME framework prescribing a longer minimum contribution lock-in and a phased release mechanism for excess promoter holding that has no Mainboard equivalent.

This article examines each dimension of that framework: promoter identification, the eligibility test for minimum promoters’ contribution, the Mainboard and SME lock-in regimes and the circumstances in which they diverge and the depository implementation mechanism, including the change introduced by the March 2026 amendment to Regulation 17 of the SEBI ICDR Regulations, 2018.

Promoter identification as the starting point of the lock-in analysis

Before the lock-in framework can be applied in practice, the first step is to identify who the promoters of the issuer are.

Regulation 2(1)(oo) of the SEBI ICDR Regulations, 2018 defines a promoter to include: (a) a person who has been named as a promoter in the offer document; (b) a person who has control over the affairs of the issuer; and (c) a person under whose advice, directions, or instructions the board of directors is accustomed to act. Regulation 2(1)(pp) separately defines the promoter group, capturing immediate relatives and entities linked to the promoter.

In practice, a person is named as a promoter in the offer document upon satisfaction of the control or board-influence test under limbs (b) and (c). Therefore, the named disclosure in an offer document is generally a consequence of that exercise, not an independent classification ground. Control over an issuer may arise through shareholding, voting rights, the ability to appoint the majority of the board, or contractual governance arrangements. A person who does not appear on a shareholding list could still qualify as a promoter if control is exercised through other mechanisms. The third limb, board influence, extends the parameter further. A person under whose advice or directions the board is accustomed to act upon falls within the definition even if their formal shareholding is low or nominal.

The depth and complexity of promoter classification, particularly the control and influence-based test, go well beyond what this article addresses. We have examined those questions at length in a two-part series – The Promoter Paradox: Mapping Control and Disclosure in India – Part I and The Promoter Paradox: Classification, Control and Compliance in Practice – Part II. Those articles cover the judicial evolution of control, the distinction between proactive and protective rights, and SEBI’s substance-over-form approach in offer document review. Readers who need to work through the classification question before applying the lock-in framework will find those pieces the appropriate starting point.

For this article, the issue of promoter and promoter group identification and classification is assumed to be settled.

Lock-in as a statutory restriction on post-IPO transferability

Lock-in is a statutory restriction on the transfer of specified securities for a prescribed period following an IPO. It operates as a legal obligation on the holder of those securities, distinct from any contractual arrangement between the issuer and its shareholders. The lock-in framework is set out under Regulation 16 for Mainboard IPOs and Regulation 238 for SME IPOs under the SEBI ICDR Regulations, 2018, with each provision addressing a distinct lock-in period.

For promoters, the restriction operates through two separate buckets:

The first bucket is the Minimum Promoters’ Contribution (MPC), being a mandatory holding of at least 20% of the post-issue capital drawn from eligible promoter securities. Where promoters cannot meet this threshold from their own holding, specified categories of investors may contribute toward the shortfall without being classified as promoters, subject to a cap of 10% of post-issue capital, and securities so contributed carry the same lock-in as MPC.

The second bucket is excess promoter holding, comprising all promoter securities above the MPC threshold.

Both buckets carry separate lock-in periods and must be separately computed and disclosed in the offer document. Treating the total promoter holding as a single pool with one uniform lock-in period produces inconsistencies across the offer document, the cap table, and the depository records, and typically draws observations from the regulator and the stock exchanges.

Lock-in also extends to pre-issue capital held by persons other than promoters. Regulation 17 for Mainboard IPOs and Regulation 239 for SME IPOs restrict the transfer of all such securities from the date of IPO allotment. This is a parallel obligation, distinct from the promoter lock-in buckets, and must be separately analysed, disclosed in the offer document, and implemented at the depository.

On the operational side, lock-in is implemented through a formal depository instruction marking the identified securities as restricted for the applicable period. A longstanding practical difficulty arose where pre-IPO shares held by non-promoters were pledged: the depository system was technically unable to create a standard lock-in marking over pledged securities, leaving a gap between the regulatory requirement and its implementation. The March 2026 amendment to the SEBI ICDR Regulations, 2018 addresses this by inserting a new sub-regulation (2) into Regulation 17, requiring depositories to record pledged shares held by non-promoters as non-transferable for the full duration of the applicable lock-in period, upon receipt of instructions from the issuer. If the pledge is subsequently invoked or released, the restriction continues for the remainder of the lock-in period. The amendment provides a clearer mechanism through which the lock-in obligation is recorded, without altering the underlying legal restriction or the duration of the lock-in period.

Why the SEBI ICDR Regulations require lock-in?

Pre-IPO shareholders receive listing liquidity when the company enters the public market. Without a lock-in framework, promoters could liquidate their entire holding through the exchange immediately after listing, leaving public investors with no assurance of promoter continuity in the business they have subscribed to.

The SEBI ICDR lock-in framework addresses this through three connected regulatory objectives. First, public investors entering at the IPO stage receive assurance that promoters cannot immediately exit. Second, promoters remain economically tied to the issuer during the early post-listing period, when the issuer is adjusting to public market discipline and investor expectations. Third, early promoter-led supply is moderated while price discovery is taking place, reducing the risk of listing-day volatility from concentrated insider selling.

These objectives explain why Mainboard and SME IPOs attract different lock-in periods. An SME issuer is typically at an earlier stage of development, with a smaller public float and lower secondary market liquidity than a Mainboard issuer. A longer promoter lock-in period reflects the investor protection rationale more strongly in that context.

Minimum Promoters’ Contribution: the anchor of the promoter lock-in framework

For both Mainboard and SME IPOs, promoters are required to hold not less than 20% of the post-issue capital as MPC. Post-issue capital is computed by adding the fresh issue shares to the pre-issue capital. 20 % of that figure is the MPC quantum.

| Bucket | Meaning | Lock-in period |

|---|---|---|

| Minimum Promoters’ Contribution (MPC) | Mandatory 20% of post-issue capital drawn from eligible promoter securities. | 18 months (Mainboard standard) or 3 years (SME and Mainboard capex-heavy). |

Identifying the MPC quantum is only the first step. Before any lock-in period is applied, the securities proposed for MPC must pass an eligibility test. That is where many cap table reviews go wrong.

Eligibility of securities for MPC: the test before the timeline

Before the lock-in period can be applied to the MPC bucket, the promoter’s securities must first be tested for eligibility to determine which of them can form part of the minimum contribution. This determination of eligible securities is important because a security that fails the eligibility test cannot be allocated to the MPC bucket, and placing a depository lock-in marking over an ineligible security does not cure the shortfall or satisfy the regulatory requirement.

The correct approach is therefore to first identify all promoter securities, test each against the eligibility criteria as provided under Regulation 15 for Mainboard IPOs and Regulation 237 for SME IPOs, establish the eligible pool, and only then allocate the required 20% of post-issue capital as MPC and apply the applicable lock-in period. Eligibility is a condition precedent to the lock-in analysis, and errors at this stage do not self-correct at the depository implementation stage.

Securities that cannot form part of MPC

The following categories of securities, subject to some exception, are ineligible for MPC under Regulation 15 (Mainboard) and Regulation 237 (SME) of the SEBI ICDR Regulations, 2018:

| Sr. No. | Category |

|---|---|

| 1. | Securities acquired for consideration other than cash where revaluation of assets or capitalisation of intangible assets is involved, acquired during the preceding three years |

| 2. | Bonus shares issued by utilisation of revaluation reserves or unrealised profits, or bonus shares issued against equity shares that are themselves ineligible for MPC, acquired during the preceding three years |

| 3. | Securities acquired during the preceding one year at a price lower than the IPO offer price |

| 4. | Securities allotted at a price less than the issue price against funds brought in during the preceding one year, in the case of an issuer formed by conversion of a partnership firm or LLP where the partners are the promoters and there is no change in management |

| 5. | Pledged securities |

From a diligence perspective, MPC eligibility cannot be confirmed from the latest capitalization table alone. Each promoter security proposed to be counted towards MPC should be traced through the issuer’s capital history, including allotment and transfer records from incorporation, corporate approvals, statutory filings and registers, valuation and consideration records, reserve utilization for bonus issuances, pledge or encumbrance records, and any scheme of arrangement, court order, tribunal order or regulatory approval under which the shares may have been issued.

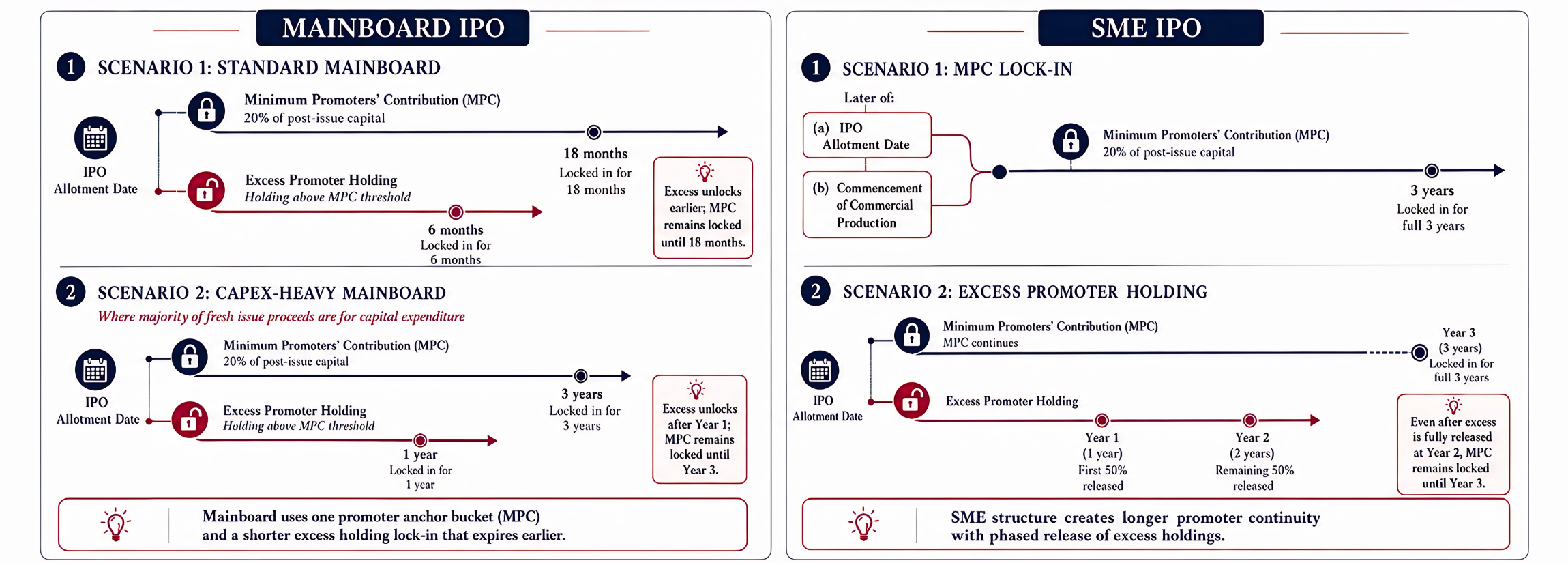

Mainboard IPOs: standard lock-in and the capex-linked extension

For an unlisted issuer going for a Mainboard IPO, Regulation 16(a) of the SEBI ICDR Regulations, 2018 requires MPC to be locked in for 18 months. Regulation 16(b) separately locks in excess promoter holding for 6 months. Both periods run from the date of allotment in IPO and must be disclosed separately in the offer document.

These standard periods extend where the majority of fresh issue proceeds is proposed for capital expenditure. The trigger is the object of the issue section of the offer document: where capital expenditure accounts for the majority of fresh issue proceeds, tested on fresh issue proceeds alone and excluding OFS proceeds, the proviso to Regulation 16(a) extends the MPC lock-in to 3 years and the proviso to Regulation 16(b) extends the excess promoter holding lock-in to 1 year. However, the lock-in on pre-issue capital held by persons other than promoters remains unchanged at 6 months under Regulation 17, irrespective of whether the majority of fresh issue proceeds is proposed for capital expenditure.

| Mainboard bucket | Standard lock-in | Capex-heavy lock-in |

|---|---|---|

| MPC: 20% of post-issue capital | 18 months | 3 years |

| Excess promoter holding | 6 months | 1 year |

| Non-promoter pre-issue capital | 6 months | 6 months |

SME IPOs: longer promoter continuity and phased release of excess holding

The SME framework under Chapter IX of the SEBI ICDR Regulations, 2018 operates on a different structure: the MPC lock-in runs from a distinct trigger point, and excess promoter holding is released in two phased tranches rather than as a single block on a fixed date. While the 20% MPC requirement is the same as under the Mainboard framework, Regulation 238(a) requires the MPC to be locked in for 3 years, and this period runs from whichever of two dates is later: commencement of commercial production or the date of allotment in the IPO.

This distinction is particularly relevant for manufacturing SME issuers raising funds to set up or expand production capacity.

Where allotment and commencement of commercial production do not coincide, the 3-year lock-in clock starts from the later of the two dates. If allotment occurs in January and commercial production is expected to commence in June, the lock-in period will begin from June.

The offer document must therefore identify the expected commencement date wherever commercial production is a future event, and the depository instruction must be computed and recorded from that later date. For issuers already in commercial production at the time of the IPO, allotment will ordinarily be the later date and the question does not arise in the same way. Further, Chapter IX does not provide for an extended lock-in period where the objects of the issue include capital expenditure. The 3-year MPC lock-in under Regulation 238(a) applies as the base rule, regardless of the objects of the fresh issue.

Under Regulation 238(b), excess promoter holding above the MPC in an SME IPO is released in two equal tranches from the date of allotment: the first 50% becomes transferable after 1 year and the remaining 50% after 2 years. The offer document must reflect this phased structure separately for each tranche, specifying the number of securities and the applicable lock-in period. A composite disclosure stating that excess promoter holding is locked in for 2 years as a single block is incorrect and does not satisfy the requirement under Regulation 238(b).

| SME bucket | Lock-in period | Trigger point |

|---|---|---|

| MPC: 20% of post-issue capital | 3 years | Commencement of commercial production or IPO allotment, whichever is later |

| Excess promoter holding, first tranche (50%) | 1 year | Date of allotment in the IPO |

| Excess promoter holding, second tranche (50%) | 2 years | Date of allotment in the IPO |

The difference between the Mainboard and SME frameworks is most visible in the treatment of excess promoter holding. In a standard Mainboard IPO, the entire excess promoter holding is released from lock-in upon expiry of 6 months from the date of allotment. However, under the SME framework, there is no single release date. The 50% of excess promoter holding is released after 1 year and the remaining 50% is released after 2 years, from the date of allotment.

Illustrative comparison of MPC, Excess promoter holding, triggering dates and release timelines

Non-promoter pre-issue capital: the parallel lock-in that is often missed

Lock-in under the SEBI ICDR Regulations, 2018 extends beyond promoters. Regulation 17 for Mainboard IPOs and Regulation 239 for SME IPOs separately restrict the transfer of pre-issue capital held by persons other than promoters, with the lock-in period running from the date of IPO allotment for 6 months in a Mainboard IPO and 1 year in an SME IPO. This is a parallel obligation that must be separately analysed, disclosed in the offer document, and implemented at the depository. The category of persons to whom it applies is wider than a standard cap table review captures: it includes early investors, seed-stage shareholders, immediate relatives of promoters forming part of the promoter group under Regulation 2(1)(pp), and persons who received pre-IPO shares through secondary transactions.

Where non-promoter pre-issue shares are pledged, the issuer faces a practical problem. Standard depository lock-in cannot be created over pledged securities. Before the March 2026 amendment, the only way to comply was to first release the pledge, which required the shareholder to obtain consent from the lender. In companies with a large number of pre-issue shareholders, some shareholders could not be traced, some maybe uncooperative, and the encumbrance sat entirely outside the issuer’s control. The result was a last-mile compliance gap that could delay filings and disrupt IPO timelines.

The March 2026 amendment to Regulation 17 resolves this difficulty by requiring depositories to mark such pledged shares as non-transferable for the full duration of the applicable lock-in period, upon receipt of instructions from the issuer, with the restriction continuing for the remainder of the lock-in period even if the pledge is subsequently invoked or released.

Anchor investor lock-in: a separate and shorter restriction

An anchor investor as defined under Regulation 2(1)(c) of the SEBI ICDR Regulations, 2018 is a qualified institutional buyer who applies for a value of at least ₹10 crore in a Mainboard IPO or at least ₹2 crore in an SME IPO through the book-building process. Anchor investors are allotted shares one day before the IPO opens for public subscription.

Their lock-in is governed by Schedule XIII, Part A of the SEBI ICDR Regulations, 2018. Of the total shares allotted to an anchor investor, 50% are locked in for 30 days from the date of allotment and the remaining 50% are locked in for 90 days from the date of allotment.

The anchor investor lock-in is shorter than both the promoter and non-promoter pre-issue lock-in periods and serves a different purpose. It ensures that anchor investors, whose early participation supports price discovery before the IPO opens to the public, do not exit immediately post-listing.

Illustration: applying the lock-in framework to a single capital structure

The following illustration applies the framework across three IPO scenarios on the same capital structure. The lock-in period changes with each route. The analytical sequence does not.

XYZ Limited is proposing an IPO. The company has two promoters: Promoter A and Promoter B.

The capital structure

| Particular | Number of shares |

|---|---|

| Pre-issue paid-up capital | 10,000 |

| Pre-issue Shares held by Promoter A | 5,600 |

| Pre-issue Shares held by Promoter B | 1,400 |

| Pre-issue Total Promoter Holding | 7,000 |

| Pre-issue Non-promoter Holding | 3,000 |

| Fresh issue in IPO | 4,000 |

| Post-issue paid-up capital | 14,000 |

Assumption: All shares are fully paid-up and no outstanding convertible securities, warrants, or partly paid shares require adjustment to the post-issue capital.

Step 1: Compute MPC

Post-issue capital = 10,000 (pre-issue) + 4,000 (fresh issue) = 14,000 shares.

MPC = 20% of 14,000 = 2,800 shares.

These 2,800 shares must comprise of eligible promoter securities as per Regulation 15 (Mainboard) or Regulation 237 (SME)

Step 2: Allocate MPC between promoters

| Promoter | Total holding | MPC contribution |

|---|---|---|

| Promoter A | 5,600 | 2,240 |

| Promoter B | 1,400 | 560 |

| Total | 7,000 | 2,800 |

Step 3: Compute excess promoter holding

Excess promoter holding = 7,000 – 2,800 = 4,200 shares.

| Bucket | Shares |

|---|---|

| Total promoter holding (A) | 7,000 |

| MPC (B) | 2,800 |

| Excess promoter holding (A-C) | 4,200 |

| Non-promoter pre-issue holding (D) | 3,000 |

Outcome A: Mainboard IPO, standard case

The majority of fresh issue proceeds is not proposed for capital expenditure.

| Lock-in bucket | Shares | Lock-in period (from the date of allotment in IPO) |

|---|---|---|

| Minimum promoter contribution | 2,800 | 18 months |

| Excess promoter holding | 4,200 | 6 months |

| Non-promoter pre-issue capital | 3,000 | 6 months |

Outcome B: Mainboard IPO, capital expenditure case

The majority of fresh issue proceeds is proposed for capital expenditure. For example, ₹60 crore of ₹100 crore fresh issue proceeds is proposed for land, plant and machinery, and civil works.

| Lock-in bucket | Shares | Lock-in period (from the date of allotment in IPO) |

|---|---|---|

| Minimum promoter contribution | 2,800 | 3 years |

| Excess promoter holding | 4,200 | 1 year |

| Non-promoter pre-issue capital | 3,000 | 6 months |

Outcome C: SME IPO

The issuer proposes its IPO on the SME platform. The SME framework under Chapter IX applies.

| Lock-in bucket | Shares | Lock-in period |

|---|---|---|

| Minimum promoter contribution | 2,800 | 3 years from commencement of commercial production or from the date of allotment in IPO, whichever is later |

| Excess promoter holding, first tranche (50%) | 2,100 | 1 year from the date of allotment in IPO |

| Excess promoter holding, second tranche (50%) | 2,100 | 2 years from the date of allotment in IPO |

| Non-promoter pre-issue capital | 3,000 | 1 year from the date of allotment in IPO |

Mainboard & SME Comparison: same capital structure, three outcomes

| Lock-in bucket | Mainboard IPO | SME IPO | |

|---|---|---|---|

| Standard Issue | Capex-heavy Issue | ||

| MPC (2,800 shares) | 18 months from the date of allotment in IPO | 3 years from the date of allotment in IPO | 3 years from commencement of commercial production or allotment, whichever is later |

| Excess holding (4,200 shares) | 6 months from the date of allotment in IPO | 1 year from the date of allotment in IPO | 2,100 for 1 year; 2,100 for 2 years from the date of allotment in IPO |

| Non-promoter pre-issue (3,000 shares) | 6 months from the date of allotment in IPO | 6 months from the date of allotment in IPO | 1 year from the date of allotment in IPO |

Conclusion

Lock-in is not merely an analytical exercise, it is the mechanism through which public investors receive assurance that the promoters who built the business will remain accountable to it through the early and often most consequential phase of its life as a listed entity. That assurance is only as strong as the analysis that underpins it, and that analysis is sequential: promoter identification determines who is subject to the obligation, eligibility testing determines which of their securities can form part of the minimum contribution, and bucket allocation, framework selection, and period assignment follow in that order before the depository instruction gives effect to the entire position. A lock-in analysis that begins at the depository stage and works backwards will almost certainly produce a position that cannot be sustained through offer document review.

A lock-in analysis conducted early, on a complete allotment history and a properly classified cap table, resolves questions that become significantly harder to address once the offer document is in advanced shape, because the Mainboard and SME frameworks impose materially different obligations on the same capital structure, the capex exception can extend lock-in periods considerably, and the non-promoter pre-issue category is wider than a standard shareholding review typically captures, with each of these carrying direct consequences for the offer document disclosures, the depository instruction, and the issuer’s post-listing obligations. Getting the lock-in position right is a function of the analysis conducted before the offer document is filed, and the rigour of that determination is what separates a compliant disclosure from one that unravels under regulatory scrutiny.