What is Purchase Price Allocation?

Purchase Price Allocation is a practice in which an acquirer allocates the purchase price into the assets and liabilities of the target company acquired in the transaction in case of acquisition accounting.

In other words, PPA is an acquisition accounting process of assigning a fair value to all of the acquired assets and liabilities assumed by the target company. PPA is a critical step in accounting reporting after the completion of a merger or acquisition.

The IFRS or other currently accepted accounting standards require employing the purchase price allocation method for any type of business combination deal, including both mergers and acquisitions. It should be noted that past accounting standards required purchase price allocation only in acquisition deals.

Importance

- Accurate Financial Reporting: PPA ensures the accurate reporting of the acquired company’s assets and liabilities on the acquirer’s financial statements. This information is crucial for investors, stakeholders, and regulatory bodies to evaluate the financial impact of the acquisition.

- Compliance with Accounting Standards: PPA is essential for complying with accounting standards such as Indian Accounting Standards (Ind AS) or International Financial Reporting Standards (IFRS). These standards require acquirers to allocate the purchase price based on the fair value of the acquired assets and liabilities.

- Tax Planning and Implications: PPA affects the tax treatment of various assets and liabilities acquired in an M&A transaction. By accurately allocating the purchase price, acquirers can optimize tax planning strategies and manage tax implications effectively.

- Investor Decision-making: PPA provides a clear understanding of the value attributed to different assets and liabilities. This information is valuable for investors in making informed decisions regarding the investment potential and performance of the acquiring company.

Regulatory Standpoint

Ind AS 103 or Indian Accounting Standard 103, is a financial reporting standard issued by the Institute of Chartered Accountants of India (ICAI) that provides guidance on accounting for business combinations. It is applicable to entities that prepare financial statements in accordance with Indian Accounting Standards (Ind AS), which are converged with International Financial Reporting Standards (IFRS).

The key considerations under the Indian regulatory framework for PPA include:

- Fair Value Assessment: Indian accounting standards require the use of fair value to allocate the purchase price. Acquirers must determine the fair value of identifiable assets and liabilities acquired in the business combination, adhering to the prescribed valuation techniques.

- Valuation Expertise: The Companies Act mandates the involvement of registered valuers for determining the fair value of assets and liabilities. These valuers possess the necessary expertise and independence to assess the fair value of different classes of assets, such as tangible assets, intangible assets, and contingent liabilities.

- Disclosure and Reporting: Indian regulations emphasize transparent disclosure and reporting of PPA-related information. Acquirers must provide detailed information on the allocation of the purchase price in their financial statements and accompanying notes, ensuring compliance with applicable accounting standards and statutory requirements.

- Regulatory Scrutiny: PPA is subject to scrutiny by regulatory bodies such as the Ministry of Corporate Affairs (MCA) and the Securities and Exchange Board of India (SEBI). These bodies monitor compliance with accounting standards, valuations, and disclosures, ensuring the reliability and accuracy of financial statements.

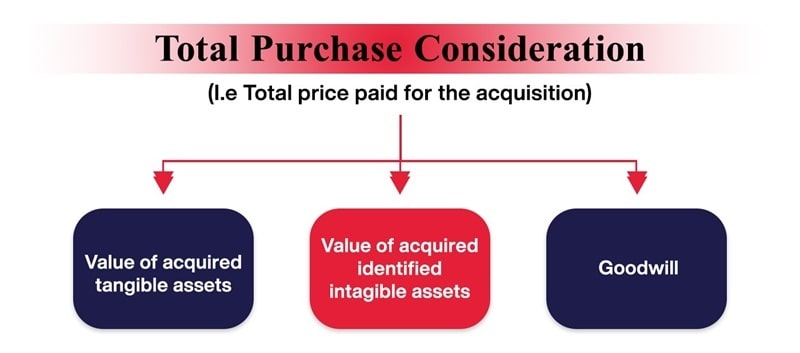

Components of Purchase Price Allocation

Purchase price allocation primarily consists of the following components:

Net identifiable assets

Net identifiable assets refer to the total value of the assets of the target company, less the total amount of its liabilities. It should be noted that the “identifiable assets” are those with a certain value at a given point of time and whose benefits can be recognized and reasonably quantified.

The net identifiable assets represent the book value of assets on the balance sheet of the target company. Identifiable assets may include both tangible and intangible assets.

If an intangible asset meets either or both criteria below, it can be recognized separately from goodwill and be valued at fair value.

- The intangible asset is related to contractual or legal rights, even if the rights are not separable.

- The intangible asset can be separated from the acquisition target and be transferred or sold without restrictions regarding transferability.

Write-up (Fair Value Adjustments)

A write-up is an adjusting increase to the book value of an asset that is made only when the asset’s carrying value is less than its fair market value. The write-up amount is determined when an independent business valuer completes the assessment of the fair market value of the assets of the target company.

The acquirer’s balance sheet will contain the target’s assets, which should carry their adjusted fair values upon transaction close.

The assets most likely to be write up (or write down) are as follows:

- Property, Plant & Equipment (PPE)

- Inventory

- Intangible Assets

Further, the fair value of the tangible assets – especially, property, plant & equipment (PPE) serves as the new basis for the depreciation schedule (i.e., spreading out the capital expenditure across the useful life assumption).

Like that, the acquired intangible assets are amortized over their expected useful lives, if applicable.

Both depreciation and amortization can have a major impact on the acquirer’s future net income (and earnings per share) figures.

Following a transaction with increased future depreciation and amortization expenses, the acquirer’s net income tends to fall in the initial periods after the transaction closes.

Goodwill

Goodwill is the excess amount paid over a target company’s net asset value. It represents the difference between the purchase price and the fair market value of the company’s assets and liabilities. Goodwill is important for accounting purposes, as both US GAAP and IFRS require companies to reassess and potentially adjust recorded goodwill annually. It serves as a “plug” in the accounting equation to maintain balance. Goodwill is not depreciated but can be amortized over time. Acquisition-related costs are not included in the purchase price allocation. Goodwill is subject to impairment testing annually, although private companies have modified rules. Valuing goodwill is part of the purchase price allocation process and falls under goodwill accounting.

Effect of PPA

PPA has a significant impact on the financial statements of the acquiring company after a business combination. The allocation of the purchase price to individual assets and liabilities acquired affects various elements of the financial statements, including the balance sheet, income statement, and cash flow statement. Here’s a breakdown of the effects of PPA on each of these financial statements:

Balance Sheet:

Assets: PPA impacts the values assigned to tangible assets (such as property, plant, and equipment) and intangible assets (such as patents, trademarks, customer relationships). The fair value of these assets, determined through the valuation process, replaces the historical book values.

Liabilities: PPA also affects the recognition and measurement of acquired liabilities. Contingent liabilities and contractual obligations are assessed, and their fair values are recorded on the balance sheet.

Goodwill: Any excess of the purchase price over the fair value of identified assets and liabilities is allocated as goodwill. Goodwill represents the future economic benefits expected from the acquisition but cannot be separately identified or valued.

Income Statement:

Amortization and Depreciation: PPA impacts the amortization of intangible assets with finite useful lives and the depreciation of tangible assets. The allocated values determine the annual amortization and depreciation expenses reported on the income statement.

Impairment: The fair value assessment performed during PPA helps identify any impairment of assets acquired. If the fair value is lower than the carrying value, an impairment loss is recognized, impacting the income statement.

Fair Value Adjustments: PPA may lead to fair value adjustments related to contingent consideration, deferred revenue, or other financial items. These adjustments impact revenue recognition and can result in changes to future revenue and expenses.

Cash Flow Statement:

Operating Activities: PPA affects cash flows from operating activities by influencing the reported net income through changes in depreciation, amortization, impairment charges, and fair value adjustments.

Investing Activities: The purchase price allocated to individual assets and liabilities impacts the cash flow from investing activities, particularly in relation to acquisitions or business combinations.

Financing Activities: If the purchase price includes assumed debt or contingent liabilities, it can affect the cash flows from financing activities, such as interest payments or changes in debt obligations.

Reasons for PPA Valuation:

PPA valuation is done for several reasons, including:

1. Financial Reporting: PPA valuation is primarily performed to determine the fair value of assets and liabilities acquired in a business combination. This valuation is crucial for accurately reporting the financial impact of the acquisition on the acquirer’s financial statements. It helps in presenting a true and fair view of the acquired company’s assets, liabilities, and equity.

2. Compliance with Accounting Standards: PPA valuation is essential for complying with accounting standards such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). These standards require acquirers to allocate the purchase price based on the fair value of the acquired assets and liabilities. By following the prescribed valuation methodologies and techniques, acquirers ensure adherence to the accounting principles and standards.

3. Price Allocation into Assets & Liabilities: PPA valuation enables the allocation of the purchase price to individual assets and liabilities acquired in the business combination. It provides a basis for determining the value attributed to tangible assets, intangible assets, and liabilities. This allocation is crucial for financial reporting, taxation, and compliance purposes, as it impacts the balance sheet, income statement, and cash flow statement of the acquiring company.

4. Tax Planning and Implications: PPA valuation affects the tax treatment of various assets and liabilities acquired in an M&A transaction. By accurately valuing and allocating the purchase price, acquirers can optimize tax planning strategies. Different tax implications arise based on the valuation and classification of assets and liabilities, impacting tax deductions, depreciation, and amortization expenses.

5. Investor Decision-making: PPA valuation provides valuable information to investors and stakeholders. It helps them understand the value attributed to different assets and liabilities, which aids in assessing the financial position and potential of the acquiring company. Investors rely on this information to make informed decisions regarding investment opportunities, financial performance, and future growth prospects.

Regulatory Compliance: PPA valuation ensures compliance with regulatory requirements and guidelines. Regulatory bodies such as the Securities and Exchange Commission (SEC) in the United States or the Securities and Exchange Board of India (SEBI) in India require accurate financial reporting and disclosure of acquisition-related information. PPA valuation helps meet these compliance obligations by providing transparent and reliable valuation of acquired assets and liabilities.

Example of Purchase Price Allocation

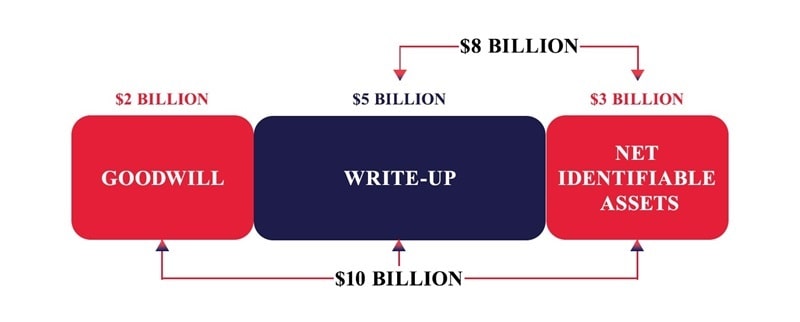

A company wishes to acquire a particular target company for a reason. After much negotiation, a purchase price of $10 billion has been agreed upon by both sides. As of the acquisition date, the target company reported net identifiable assets of $3 billion (Assets $7 billion – Liabilities $4 billion) on its own balance sheet.

Before the target company can complete the acquisition, the target must appraise the assets and liabilities being acquired to determine their Fair Value (“FV”), the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The acquirer hires a valuer who reports that the FV of the net assets is $8 billion.

The figure below walks through the difference between the three values ($3 billion, $8 billion, and $10 billion).

The difference between the $3 and $8 is $5B in write-up — the values of the net identifiable assets are in effect increased to 2.5 times the value reported on the original balance sheet. The difference between the $8 billion and $10 billion is $2 billion in goodwill acquired through the transaction, the excess of the purchase price paid over the FV of the net identifiable assets acquired.

Finally, the acquirer adds both the value of the written-up assets ($8 billion) as well as the goodwill ($2 billion) onto the balance sheet, for a total of $10 billion in new net assets on the acquirer’s balance sheet.

The process of conducting the appraisal, reporting the FV of the assets and liabilities, the allocation of the net identifiable assets from the old balance sheet price to the FV and the determination of the goodwill in the transaction, is referred to as the PPA process. It should be noted that a purchase price may be less than the target’s balance sheet value for a variety of reasons, which can lend itself to a write-down of net assets.

Purchase Price Allocation (PPA) is a critical process in M&A transactions, enabling the accurate reporting and disclosure of the financial impact of acquisitions. In India, the regulatory framework surrounding PPA, guided by the Companies Act and Ind AS, ensures transparency, compliance, and reliable financial reporting. Adhering to the prescribed guidelines and involving qualified valuers is crucial to conducting PPA in accordance with Indian regulatory requirements. By understanding and effectively implementing PPA, acquirers can enhance decision-making, optimize tax planning, and meet the expectations of stakeholders and regulatory authorities.