The Reserve Bank of India (RBI) in its Annual Policy 2010-2011 had announced that companies which have their assets predominantly as investments in shares for holding stake in group companies but not for trading, and also do not carry on any other financial activity justifiably deserve a differential treatment in the regulatory prescription applicable to Non-Banking Financial Companies which are non-deposit taking and systemically important.

Accordingly, RBI in year 2011 introduced the concept of the Core Investment Company (“CIC”). CIC is defined as a Company where:

- not less than 90% of its assets are in investments in shares, debt, loans in group companies for the purpose of holding stake in the investee companies

- Atleast 60% of its net assets is in form in equity of group companies

- not trading in these shares except for block sale (to dilute or divest holding)

- not carrying on any other financial activities,

- not holding / accepting public deposits

But since its introduction, the concept of CIC’s which was originally incorporated in order to serve as corporate benefactor, has failed to serve its purpose but has resulted in derogating the corporate governance regime in India. In this article, we have discussed regulatory provisions governing CICs along with the issues engulfing them. Further the recommendations of Working Group constituted by the RBI to examine the current regulatory framework of CIC including but not limited to assess the appropriateness and suggest the changes incl. governance etc., are also discussed.

A CIC having an asset size of Rs.100 crore & above and which has accessed public funds would be treated as systemically important core investment company (CIC-ND-SI). In case there is more than one CIC in a group, assets size shall be taken on consolidated basis and further registration will be required to obtained by every CIC which has accessed public funds and whose aggregate assets size is Rs 100 crore or more. Every CIC-ND-SI is required to obtain Certificate of Registration (COR) from RBI under Section 45-IA of the Reserve Bank of India Act, 1934. However, CIC-ND-SI is not required to fulfill the criteria of having minimum net owned fund (i.e. rupees two crores) subject to adherence to other prudential norms. The CIC registered with RBI is subject to the Master Directions – Core Investment Companies (Reserve Bank) Directions, 2016 (“CIC Directions”) wherein such CIC is required to adhere to certain prudential norms among other requirements.

A. Prudential Norms

- Capital Requirement

Every CIC-ND-SI shall ensure that at all times it maintains a minimum Capital Ratio whereby its Adjusted Net Worth (“ANW”) shall not be less than 30% of its aggregate risk weighted assets on balance sheet and risk adjusted value of off-balance sheet items as on the date of the last audited balance sheet as at the end of the financial year.

(Adjusted Net Worth means Paid Up equity capital, compulsory convertible preference shares, free reserves, securities premium, capital reserves reduced by accumulated losses, tangible assets and deferred revenue expenditure further increased by 50% increase in the value of quoted investment and in case of diminution in the Investment, 100% value shall be reduced)

- Leverage Ratio

Every CIC-ND-SI shall ensure that its outside liabilities at all times shall not exceed 2.5 times its ANW as on the date of the last audited balance sheet.

(Leverage ratio is calculated as total borrowings to adjusted net worth)

B. Other requirements

When the directions governing CIC were first issued by the RBI in the year 2011, the CIC-ND-SI was not subject to any kind of governance norms, formation of any policy/ framework, asset classification, provisioning requirements, liquidity risk guidelines, etc. However, over a period of time, the RBI has tightened the norms over CIC-ND-SI, which are as follows:

- Policy on demand/ call loans

The Board of Directors of every CIC-ND-SI granting/intending to grant demand/call loans shall frame a policy for the company and implement the same.

- Asset classification

Every CIC-ND-SI shall, after taking into account the degree of well-defined credit weaknesses and extent of dependence on collateral security for realisation, classify its lease/hire purchase assets, loans and advances and any other form of credit into the following classes, namely:

- Provisioning Requirement

Every CIC-ND-SI shall, after taking into account the time lag between an account becoming non-performing, its recognition as such, the realisation of the security and the erosion over time in the value of security charged, make provision against sub-standard assets, doubtful assets and loss assets.

Further, the CIC-ND-SI is required to disclose in its balance sheet the provisions it has made against assets.

- Information to be furnished to RBI

Every CIC-ND-SI is required to inform the change in its registered office, change in the directors, change in auditors, etc., to the RBI.

- Acquisition / Transfer of Control

- Private Placement through Non-Convertible Debentures (NCDs)

- Know Your Customer (KYC)

- Insurance Business

(i) Standard assets;

(ii) Sub-standard assets;

(iii) Doubtful assets; and

(iv) Loss assets.

Prior approval of RBI is required in case of acquisition or takeover of control of CIC-ND-SI, or where there is any change in the shareholding of 26% or more of the paid up equity capital or there is a change in the management of more than 30% of the directors excluding independent directors.

There are two sets of issuances of NCDs having maturity of more than 1 year covered under the CIC Directions i.e. one where there is a maximum subscription of less than Rs. 1 crore per investor but subject to receipt of minimum Rs. 20,000/- and the other where the minimum subscription is Rs. 1 crore or above per investor. In case of former, there is a limit of 200 investors and the subscription must be fully secured whereas in case of latter, there is no limit in the number of subscribers and there is an option to create security. Further in case of issuance of NCDs through private placement, the provisions of the Companies Act are applicable to the extent those are not in contradiction with the CIC Directions.

All CIC-ND-SIs shall be required to follow the Know Your Customer (KYC) Direction, 2016.

The RBI has issued guidelines for CIC for entering into insurance business such as eligibility criteria, risk participation, etc.

A. Legitimate and Commercial reasons

There are various legitimate reasons to have a holding CIC in the group structure such as concentration of holding, mitigation of risks, easy control of assets, succession planning, etc. Amongst other factors, following reasons can be attributed to have a holding CIC structure in a group:

- Holding companies enjoy the benefit of protection from losses, if a subsidiary company goes bankrupt, its creditors cannot legally pursue the holding company for recovery.

- Holding companies can support their subsidiaries by leveraging their balance sheet to lower the cost of much-needed operating capital.

The fact that holding company structure is preferred amongst corporates is evident from the list of registered CICs released by the RBI as on October 31, 2019, where, CICs are present in all big corporate houses such as Aditya Birla, Reliance ADAG, Tata’s L&T group, GMR etc.

B. Statutory reasons

In addition to the commercial suitability of a CIC in a group, such holding company also enjoys various exemptions under the Companies Act, 2013. Few material exemptions are as follows:

- Layers of subsidiaries

- Prior approval of public financial institutions (PFIs)

- Shareholder approval and disclosure

CICs are exempt from the provisions relating to restriction of having more than two layers of investment subsidiaries

Even if there is a default in repayment of dues to PFIs, CIC being an NBFC having the principal business of acquisition of securities can make investment in its group companies without the prior approval of PFIs.

CIC is not required to obtain the approval of its shareholders for making investment, loan or guarantee even if these are in excess of the limits i.e. 60% of paid up capital, free reserves and securities premium, or 100% of free reserves and securities premium, whichever is higher.

The above exemptions given under the Companies Act poses a serious threat not only to the CIC itself but also to the financial system

- EXCESSIVE LEVERAGE

- Complex Group Structure

- Excessive Group Companies Exposure

- Corporate Governance

- Asset Liability Mismatch

- Registration and Exemption

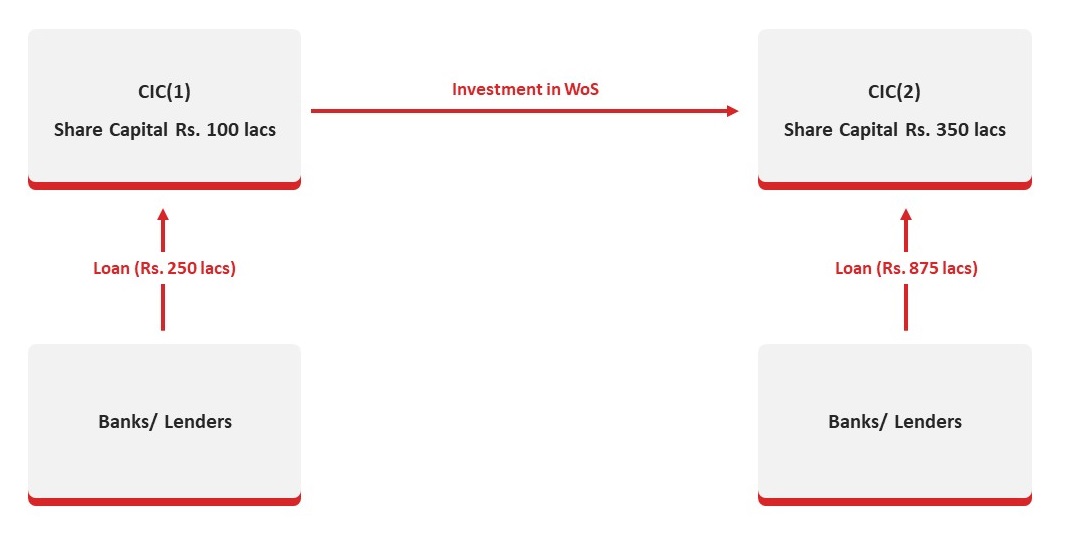

In terms of the CIC Directions, there is no restriction to have more than one CIC in the group, this enables a CIC to borrow 2.5 times of its ANW (leverage ratio) to invest in other CICs in the group, which indirectly increases the appetite to borrow funds of the other CICs. Consequently, once the leverage increases, the last CIC in the layer of group companies can avail the maximum funds from banks/ other PFIs due to increase in its ANW and invest the same in the group companies either in the form of share capital or inter corporate deposits while fulfilling the eligibility criteria of CIC (90/60). This process can be understood clearly through the following pictogram:

From the above, it may be noticed that the leverage/ exposure of the group has been increased from Rs. 250/- to Rs. 875/- even after both the CICs following the compliance of leverage ratio (i.e. 2.5 times). However, if we calculate the leverage ratio out of owned funds of the group, the actual leverage is 11.25 which is far more than what is allowed under the RBI rules. The calculation is as follows:

Total Borrowed Funds (875 + 250) divided by owned funds (Rs. 100/-)

So, by creating multiple CICs in the group, the scope of leverage at group level can be increased exponentially. The operating companies and NBFCs, if any, in the group, are eligible to raise funds directly from banks and the markets, besides getting funding from the group CICs. In this scenario, the group level leverage can become excessive and also difficult to monitor.

The leverage provided to CIC under the CIC Directions are reasonable and adequate but if misused ,it can have a material impact on the financial system of the group as a whole like what was witnessed in case of IL&FS. In such a case, any financial problem within a group company, may trigger a chain reaction and lead to liquidity issues throughout the group like a contagious disease.

The Companies Act, 2013 restricts the number of investment subsidiary companies to two and also restrict sto have more than two layers of subsidiaries under different provisions of the Act in order to ensure that large conglomerates do not render opacity to the groups in terms of ownership, controls and related party transactions. However, when it comes to NBFCs, the scope of complexity of group structure can be exacerbated since there is no such restriction that bars the existence of number of investment companies in a group and number of step-down subsidiaries specifically where the holding company is a CIC.

As per the CIC Directions, every CIC is required to invest in the group companies taking into consideration of 90/60 principles and it is also not required to deduct such investments while calculating its ANW which is contrary to the directions applicable to NBFC, where investment in the group companies in excess of 10% of its owned funds gets reduced to arrive at Net Owned Fund (i.e. not less than rupees two crores). In the below table, the distinction is made while calculating net owned fund between NBFC and CIC:

| Particulars | CIC | NBFC |

| Owned Funds | xxx | xxx |

| 50% of the unrealized appreciation in the book value of quoted investments as ay the date of last audited Balance sheet | xxx | 0.00* |

| Increase if any, in the equity share capital since the date of the last audited balance sheet | xxx | 0.00* |

| Diminution in the aggregate book value of quoted investments | (xxx) | 0.00* |

| Investment in shares subsidiaries, group companies, other NBFCs, in excess of 10% of owned funds. | 0.00* | (xxx) |

| book value of debentures, bonds, outstanding loans & advances made to or deposit with, subsidiaries and group companies, in excess 10% of owned funds. | 0.00* | (xxx) |

| Total | YYY | ZZZ |

| Adjusted Net Worth | Net Owned Fund |

(*0.00 means not allowed to consider under the RBI Directions)

From the above, it becomes clear that while CIC are also allowed to add appreciation in the market value of quoted investments in ANW, on the contrary NBFCs are neither allowed any such appreciation and even investment made by them in group in excess of 10% of owned fund is deducted from the owned funds, which consequently reduces net owned fund resulting into less scope of leverage. The aforesaid advantageous position of CIC vis-à-vis NBFC, allows promoters to create more CICs within the Group to leverage more funds from the market since the leverage power gets multiplied with every CIC in the group. The CICs generally raise funds from banks, mutual funds and other financial institutions which involve public money in form of commercial papers, non-convertible debentures and in case of default, the public money will be at stake since most of these instruments are issued as unsecured one. Even if some are secured ones, a CIC generally does not have large pool of fixed assets which can be mortgaged against bank finances and have assets mainly in form shares of subsidiaries and other group companies which are generally not sufficient enough to cover 100% security cover of the bank finance because when the holding CIC defaults, the whole assets of the group companies come under stress and recovery of loan by banks and other lenders become difficult. The lenders have no choice but to recover the money under SARFAESI Act or though Insolvency and Bankruptcy Code where the promoters lose their control over their group like in case of Essar Steel, Bhushan Steel, etc.

Good Corporate Governance is the heart and soul of the corporate regime in India. The main objective behind advocating the adherence of good corporate governance norms is to ensure increase accountability of a company so as to avoid frauds. India has witnessed failure of several corporate giants attributable to exiguous adherence to corporate governance norms. Therefore, high standards of corporate governance are of paramount importance to any organization. However, when it comes to CICs, the same is not applicable explicitly. In large number of CICs, there are no board level committees that review and monitor the transactions entered into by CICs as against the governance norms applicable to NBFCs where audit committee, nomination & remuneration committee and risk management committee are required to be constituted. As opposed to NBFCs, where a person who meets the ‘Fit and Proper criteria’ can only be appointed as a director, any person can be appointed as a director in a CIC, by following a simple procedure provided under the Companies Act.

In case of appointment of Statutory Auditors too, NBFCs are required to rotate the partner/s of the Chartered Accountant firm conducting the audit, every three years so that same partner shall not conduct audit of the company continuously for more than a period of three years and there is cooling period of subsequent three years after which rotated partner will be eligible to conduct the audit. However, in case of CIC, there is no such stipulation.

The report of Working Group constituted by RBI, also highlights the state of governance in CIC’s, where it was observed by the Working Group, that in lots of groups, directors of CIC’s have also occupied directorship in the boards of multiple companies in a group thereby seriously jeopardizing governance norm. It was also observed that several CICs had lent funds to group companies at zero percent rate of interest with bullet repayment of 3-5 years and without any credit appraisal. Hence, the position of the Boards of CICs becomes significant, particularly in mixed conglomerates, which include financial and non-financial entities, as the CIC’s board may not have the appropriate skill/capacity to monitor the diverse businesses of such large conglomerates spread across India and abroad.

In terms of the CIC Directions, the investments and all other assets of the CIC are regulated by the RBI whereas the liabilities are not so regulated since there is minimal restriction to avail public funds. The CICs generally receive dividends from its operational group companies where they are required to invest and there are no other business operations, so all its inflows are solely depending upon the profits earned by the group companies. Where the group companies operate in a capital extensive business-like insurance, infrastructure with long gestation period/ break-even point, Holding CIC generally find it difficult to raise more funds for their other group companies and accordingly they tap banks and financial institutions, to meet their funding needs. Further, the NBFCs are required to file Asset Liability Mismatch (ALM) returns on quarterly, half yearly and annually basis in order to track the mismatches and wherever the RBI deems fit, it may put such NBFCs under observation which is popularly known as ‘Prompt Corrective Action’ whereas CICs are not subject to any filing in this regard but are only required to disclose the maturity of the assets and liabilities in order to measure the future cashflows of CIC in different time buckets ranging from 1-7 days to more than 5 years. In most of balance sheet of CICs, it is found that the long terms investment made in the group companies are funded by short terms borrowings through issuance of NCDs and Commercial Papers and this has led to major mismatch between the assets & liabilities which has been one of the contentious issues in the NBFC sector.

Considering the CIC Directions, the objective thereof is to regulate only the assets of the CIC without subjecting to any stringent filters on the borrowings of CICs which may in the long run risk the financial system since CICs are at liberty to borrow funds within the leverage ratio as discussed above and pass on such funds to the loss-making group companies. In this regard, the assets of the banks recoverable from CICs are always at risks.

As per the CIC Directions, CIC’s having asset size of INR 100 crore or more and having access to public funds are required to mandatorily register with RBI which is called as CIC-ND-SI. All other CICs either having less than Rs. 100 crores assets or not having public funds are exempted from registration and such exempted CIC shall pass a board resolution that it will not, in the future, access public funds. While RBI has exempted certain class of CIC from registration, there are certain ambiguities namely whether exempted CIC are NBFCs or not; whether such CICs are also eligible to enjoy all the privileges and exemptions as are applicable to a NBFC under the Companies Act. Further, as per a direction issued by the RBI called as ‘Exemptions from the provisions of the RBI Act’ the CICs which are not systematically important are exempted from the provisions of section 45 IA of the RBI Act only (i.e. Net Owned Fund) which means that other provisions of the RBI Act are applicable to ‘exempted CIC’ such as maintenance of Reserve Fund under Section 45-IC. However, contrary to this interpretation, the FAQs available on the portal of RBI says ‘exempted CICs’ are exempted from the regulation of the RBI which means such CICs are not required to follow any RBI directions as applicable to NBFCs. Thus, stakeholders are in a toss whether to follow the foregoing Directions or FAQs since both are issued by RBI.

The RBI had constituted a Working Group vide notification dated July 03, 2019 with the sole objective of reviewing the existing regulatory and supervisory framework for CIC and recommending plausible changes therein. The Working Group in its report dated October, 2019 has recommended a plethora of changes in the existing regulatory framework, which are outlined below:

- Limiting the group structure:

- Deduction of group exposure:

- Aggregate group level Leverage:

- Obliteration of nomenclature of exempt category CICs:

- Corporate Governance Standards:

- Constitution of board level committees like Audit Committee, Risk Management Committee, Nomination Committee, Asset Liability Management Committee etc.

- Requirement with respect to preparation of consolidated financial statements of all group companies in which CICs have investment exposure.

- Appointment of Independent directors on the Board.

- Requirement of internal audit for the registered CICs.

- Restricting the appointment of executive director of a CIC in the Board of downstream unlisted entities by the respective CIC.

The number of CICs that can exist in a group should be limited to two in line with the Companies Act, 2013. This step will enable the authorities to keep a close eye on the large and intricate group structure.

While contemplating the leverage capacity of a CIC, the group exposure i.e. any contribution by CICs or other entities in a group in the form of loan or investment should be deducted from its ANW as in the case of NBFCs. This step will help in easing out the problem of over leveraging.

Further while calculating ANW, capital contribution by one CIC into another CIC in a group in excess of 10% of its owned funds shall be deducted , which is also in line with the requirement for NBFCs as explicitly mentioned hereinabove.

The working group has pointed out that problem of excessive leveraging exists since there is no limit on aggregate leverage in a group. Therefore, it is recommended that besides individual leverage for CIC, aggregate group level leverage should be demarcated in order to ensure that aggregate borrowing of a group does not exceed the limit as may be prescribed in near future.

The working group has pointed out that exempt CICs gain credibility by virtue of being ‘exempted’ by the Central Bank which inter alia, could facilitate fund raising. Therefore, it is essential that the nomenclature of exempt category CICS should be obliterated from the Core Investment Companies (Reserve Bank) Directions, 2016.

The working group observed that unlike NBFCs, no corporate governance standards are applicable on CICs. Therefore, it is recommended that the Central Bank should formulate and implement certain corporate governance norms in line with the Companies Act, 2013 and Securities and Exchange Board of India (Listing Obligations and Disclosure Requirement) which may include:

CIC, when initially introduced by the RBI, was welcomed by the corporate houses since it provides the flexibility to own operational companies through a single holding company without going for registration as NBFC and thereby saving a company from vicious compliance circle and compliance cost. However, over the period of time, the corporate houses have taken the advantage of less regulated CIC in form of indefinite exposure to group companies. As a result, a financial crisis at a CIC severely affects the liquidity position of its operational group companies resulting into a chain reaction of bank defaults. The working group constituted by RBI seems to have addressed the issues in CIC’s structure and their recommendations, if implemented will definitely have far reaching impact on strengthening the CIC framework.