Apr 23, 2026

Voluntary Quarterly Business Updates by Listed Companies: Good Practice, or a Trap of One’s Own Making in a Regulatory Grey Zone?

A growing number of Indian listed companies have adopted the practice of filing voluntary quarterly business update announcements on the BSE and NSE platforms, typically within the first few weeks of a quarter’s close, well before the formal financial results are published. These updates, which are not mandated by any specific provision of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“LODR Regulations”), have become a distinctive feature of investor communications for companies that command significant attention from both institutional and retail investors.

One may argue that the practice has emerged organically from the market’s demand for timely, regular and granular information. At the same time, this practice raises a set of layered regulatory questions that merit careful examination within the existing disclosure architecture: whether such disclosures are purely voluntary or, in certain circumstances, fall within the ambit of the continuous disclosure framework under Regulation 30 of the LODR Regulations. Whether selective operational metrics without a full profit and loss account, constitute Unpublished Price Sensitive Information (“UPSI”), and whether filing such admittedly selective information on a stock exchange is sufficient to convert it into generally available information under the SEBI (Prohibition of Insider Trading) Regulations, 2015 (“PIT Regulations”), and whether such selective disclosures could also expose the company to allegations of manipulative, fraudulent, or unfair trade practices under the SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003 (“PFUTP Regulations”)? This article examines each of these questions through the lens of applicable Indian securities law and draws on international practice for comparative context.

I. The Regulatory Framework: What the Law Actually Says

The LODR Regulations impose two categories of disclosure obligations on listed entities: periodic disclosures (financial results, shareholding patterns, corporate governance reports) and event-based disclosures under Regulation 30, which require prompt disclosure of any material event or information that may affect the price or value of securities.

Regulation 30 read with Schedule III does not operate as a closed list but classifies disclosures into Para A events (deemed material) and Para B events [where materiality is determined under Regulation 30(4)]; while approval of financial results is a material event under Para A, triggering time-bound disclosure, voluntary quarterly operational updates such as revenue run-rate, volume dispatches, or order book position do not expressly fall within these categories.

However, it is essential to appreciate the animating spirit of the LODR framework. Regulation 4(2) of the LODR Regulations lays down the broad principles of corporate governance applicable to listed entities. These principles include, prominently, the requirement that disclosures made by a listed entity be truthful, accurate, and adequate, and be made on a non-discriminatory basis, ensuring that all investors, whether institutional or retail, receive relevant information simultaneously and on equal terms. They further require that information be complete and presented in a manner that is usable and comparable, enabling informed investment decisions. These foundational values govern how all disclosures, whether mandatory or voluntary, are made and serve as overarching standards that extend beyond any specific disclosure obligation under Schedule III. A listed entity that chooses to file a voluntary quarterly update does so not in isolation from this framework, but firmly within it: the principles of Regulation 4(2) apply with equal force to a voluntary exchange filing as they do to a mandatory result announcement.

Moreover, this voluntary characterisation immediately triggers the framework under the PIT Regulations. Under Regulation 2(1)(n) of the PIT Regulations, UPSI is defined as “information, relating to a company or its securities, directly or indirectly, that is not generally available, which, upon becoming generally available, is likely to materially affect the price of the securities.” The definition includes, by way of illustration, financial results, acquisitions, mergers, de-mergers, re-organisations, etc.

The UPSI Trigger Test — A Three-Limb Analysis

Information constitutes UPSI only if it satisfies all three limbs simultaneously: (i) it must relate to the company or its securities, whether directly or indirectly; (ii) it must not be generally available; and (iii) it must be likely to materially affect the price of securities upon becoming generally available. A critical feature of this test is that the third limb “likely to materially affect” is a forward-looking, probabilistic standard. The question is not whether the information actually moved the price upon release, but whether, at the time it was in the Insiders’ possession, it was of a nature that could influence prices upon disclosure. If a company proactively publishes operational metrics via an exchange filing, the information crosses the threshold of “generally available” under Regulation 2(1)(e) of the PIT Regulations, which defines generally available information as that which is accessible to the public on a non-discriminatory basis. A stock exchange filing satisfies this test. The logical consequence is that publication extinguishes the UPSI character of the information at the moment of disclosure, but only in situations where the disclosure is complete, simultaneous, and non-selective.

This interaction between voluntary disclosures and the UPSI framework is one of the most important regulatory dynamics surrounding quarterly business updates. A company that discloses directional performance metrics through a properly filed exchange announcement effectively converts UPSI into generally available information, thereby minimizing insider trading risk for that particular information, provided the disclosure is simultaneous, non-selective, and filed through the exchange’s electronic disclosure platform (NEAPS / BSE Listing Centre).

II. What Companies Typically Disclose: The Anatomy of a Business Update

Based on exchange filings available on the BSE and NSE listing platforms, quarterly business update announcements by Indian listed companies typically fall into two broad categories: operational highlights and financial indicators.

The following table illustrates the type of information commonly disclosed, drawn from exchange filings of well-known Indian listed companies:

| Company (Illustrative Sector) | Typical Metrics Disclosed in Quarterly Updates |

|---|---|

| Large-Cap IT Services companies (e.g., Infosys, Wipro) | Revenue (in USD and INR), constant-currency growth, EBIT margin guidance update, large deal wins, headcount, attrition rate, and geographic segment performance filed simultaneously with or as part of earnings call transcripts on the exchange |

| FMCG / Consumer companies (e.g., Hindustan Unilever, Dabur) | Volume growth, value growth, distribution reach, category-wise performance, rural vs. urban split, and management commentary on demand environment typically shared via analyst / investor presentations filed on BSE/NSE |

| Banking & NBFCs (e.g., HDFC Bank, Bajaj Finance) | AUM growth, loan book size, gross NPA ratio, net interest margin trend, deposits growth, and collection efficiency often as a dedicated quarterly update filing separate from the audited financial results |

| Auto & Auto Ancillaries (e.g., Maruti Suzuki, Bajaj Auto) | Monthly and quarterly volume data (units sold by segment), export volumes, market share indicators published as monthly sales data on the exchange, which cumulatively form a quarterly picture |

| Cement / Building Materials (e.g., UltraTech Cement, Shree Cement) | Volume dispatches (million tonnes), realisation per tonne, utilisation rates, capacity expansion updates filed as business updates ahead of formal results |

It is important to note that none of the above disclosures typically include full profit and loss statements, balance sheet figures, or audited / unaudited financial results in the format prescribed under Regulation 33 of the LODR Regulations. What is shared is directional operational performance, which allows analysts and investors to form a preliminary view on the quarter without the company having published Board-approved financial results.

III. Empirical Evidence: How Markets Actually React to Voluntary Business Updates

Before delving into the legal analysis of the issue, it is important to note that the price sensitivity of voluntarily disclosed operational metrics is not merely a theoretical proposition. Market data from Q4 FY26 update filings by Indian-listed companies provide illustrative evidence that such disclosures do move stock prices.

The following table sets out the stock price reactions observed across seven companies that filed voluntary quarterly business updates in early April 2026:

| Company | Update Trigger | Last Close Before Update | First Reactive Close | First-Session Stock Move | Nifty Move (Same Window) | Excess Move vs Nifty | Read-Through |

|---|---|---|---|---|---|---|---|

| V-Mart Retail Limited | 1 Apr 2026 after-market filing; Q4 revenue ₹971 cr, +24% YoY, 12% SSSG, 29 stores opened | ₹483.20 | ₹544.90 | +12.77% | +0.15% | +12.62 pp | Rally extended to ₹626.95 by 7 Apr (+29.75% from pre-update close) |

| Avenue Supermarts Limited (DMart) | 3 Apr 2026 after-market filing; Q4 standalone revenue ₹17,204.50 cr and store count 500 | ₹4,362.20 | ₹4,551.35 | +4.33% | +1.12% | +3.21 pp | Initial pop not sticky; by 8 Apr only +0.15% above pre-update close while market moved strongly |

| Sobha Limited | 3 Apr 2026 operational update; Q4 sales value ₹20.39 bn, FY26 highest-ever annual sales | ₹1,157.50 | ₹1,221.00 | +5.46% | +1.12% | +4.34 pp | Follow-through strong; by 8 Apr stock at ₹1,292.50 (+11.73% vs pre-update close) |

| Jubilant FoodWorks Limited | 6 Apr 2026 (19:37 filing); Q4/FY26 business update — market read-through focused on weak same-store demand | ₹461.30 | ₹412.70 | -10.40% | +0.68% | -11.08 pp | By 9 Apr still -7.21% below pre-update close; absolute growth insufficient where quality disappointed |

| Lodha Developers Limited | 7 Apr 2026 pre-open filing; Q4 pre-sales ₹58.9 bn, +23% YoY, collections up, net debt down ₹8 bn | ₹711.95 | ₹718.30 | +0.89% | +0.68% | +0.22 pp | Muted same-day reaction, but by 10 Apr stock reached ₹827.75 (+16.27% from pre-update close) as full package digested |

| Puravankara Limited | 13 Apr 2026 update; Q4 sales value ₹3,547 cr, +190% YoY, collections +36%, sales area +112% | ₹195.25 | ₹215.99 | +10.62% | -0.86% | +11.49 pp | Momentum persisted; by 15 Apr stock at ₹232.69 (+19.18% from pre-update close) |

| Shanti Gold International Limited | 14 Apr 2026 update (market holiday); Q4 volume +25% YoY, revenue +120% YoY | ₹183.67 | ₹192.52 | +4.86% | +1.63% | +3.23 pp | By 16 Apr stock at ₹194.99 (+6.20% from pre-update close) |

Two patterns stand out from this data, and both carry regulatory significance.

First, companies that disclosed a fuller picture: combining revenue figures with operating metrics such as same-store sales growth, collections, sales area, or customer traction produced stronger and more sustained stock price reactions than companies that disclosed topline growth alone. The market, in other words, rewards informational completeness over selective reporting.

Second, the direction of price movement is irrelevant for determining whether information qualifies as price-sensitive; what matters is the magnitude. Jubilant FoodWorks reported revenue growth in its quarterly update, yet its stock fell by more than 10% in a single trading session as the market focused on weak store-level demand. Information that moves a stock by ten percent in one session is, by any measure, information that was likely to materially affect its price.

IV. Is This a Healthy Practice?

The case for voluntary quarterly updates is compelling. First, they reduce information asymmetry between promoters and institutional investors, on the one hand, and retail investors, on the other. When a company proactively publishes operational metrics, in accordance with the principles of truthfulness, accuracy, and non-selective disclosure enshrined in Regulation 4(2) of the LODR Regulations, it levels the playing field and reduces the incentive to selectively brief analysts in private. Second, they manage market volatility: the empirical data in Section III above demonstrate that a company that consistently shares directional data before results narrows the gap between market expectation and actual disclosure, thereby reducing the stock price volatility that accompanies formal result announcements. Third, from a governance standpoint, regular voluntary disclosure signals management confidence and builds credibility with the investor base over time.

The concerns, however, are equally substantive. The most significant risk is cherry-picking: a company may choose to disclose only favourable metrics (strong volume growth, healthy order book) while withholding adverse ones (margin compression, rising provisioning). If selective disclosure creates a materially misleading impression, it may attract regulatory scrutiny under Section 12A of the SEBI Act, 1992, which prohibits fraudulent and manipulative trade practices. Further, dissemination of information that is false or misleading, or made recklessly or carelessly, and which is designed to, or is likely to, influence the decision of investors dealing in securities, is treated as a manipulative, fraudulent, or unfair trade practice under the PFUTP Regulations. Such selective positive disclosures aimed at influencing security prices fall squarely within this prohibition, and the price-reaction data above demonstrates the scale of price impact that a curated voluntary update can produce.

A second concern relates to forward-looking statements. Some quarterly updates include management guidance or commentary on expected full-year performance. In the absence of a clear safe harbour for forward-looking statements, companies may face legal exposure if guidance turns out to be materially incorrect.

V. The UPSI Question: Does Disclosure ‘Extinguish’ Insider Trading Risk?

This is the most legally nuanced aspect of voluntary business updates and deserves careful analysis. The starting point is a principle that is sometimes obscured in practice: any operational metric that a company’s management holds internally at quarter-end constitutes UPSI before any disclosure to the market. The reason lies in the third limb of the UPSI test, “likely to materially affect the price of securities”, which carries significant analytical weight and does not require demonstrating that the price actually moved upon disclosure. It requires only that the information, by its nature and content, is susceptible to influencing prices. The empirical data in Section III above also support the reasoning that such operational metrics satisfy the “likely to materially affect” test as a matter of market reality.

The PIT Regulations establish a framework under which UPSI loses its character as “unpublished” information once it becomes “generally available.” The practical question is: if a company’s management knows that Q2 revenues will be significantly higher than market expectations, and they publish a voluntary business update disclosing the directional revenue figure on the exchange, does this act extinguish the UPSI?

The answer, under the PIT Regulations as interpreted by SEBI and the Securities Appellate Tribunal (“SAT”), is nuanced. The disclosure must be accurate, complete and not misleading. There may be situations where a voluntary disclosure only presents a part of the overall information landscape, while significant underlying aspects remain undisclosed. In such cases, a partial disclosure that highlights positive metrics but conceals adverse elements or does not present the full picture would not qualify as a proper “generally available” disclosure for the purpose of neutralising UPSI. In Future Corporate Resources Pvt. Ltd. v. SEBI (decided on December 20, 2023), the SAT observed that information would cease to be UPSI only if it is specific, adequately detailed, and made available to the general public on a non-discriminatory basis; disclosures falling short of this standard would not meet the threshold. Consequently, even voluntary operational disclosures under Regulation 30 may not, in such circumstances, neutralise the UPSI character of the underlying information.

A critical proposition that follows from the above analysis is that selective disclosure extinguishes UPSI only with respect to the specific information disclosed, leaving the UPSI character of all remaining undisclosed information fully intact.

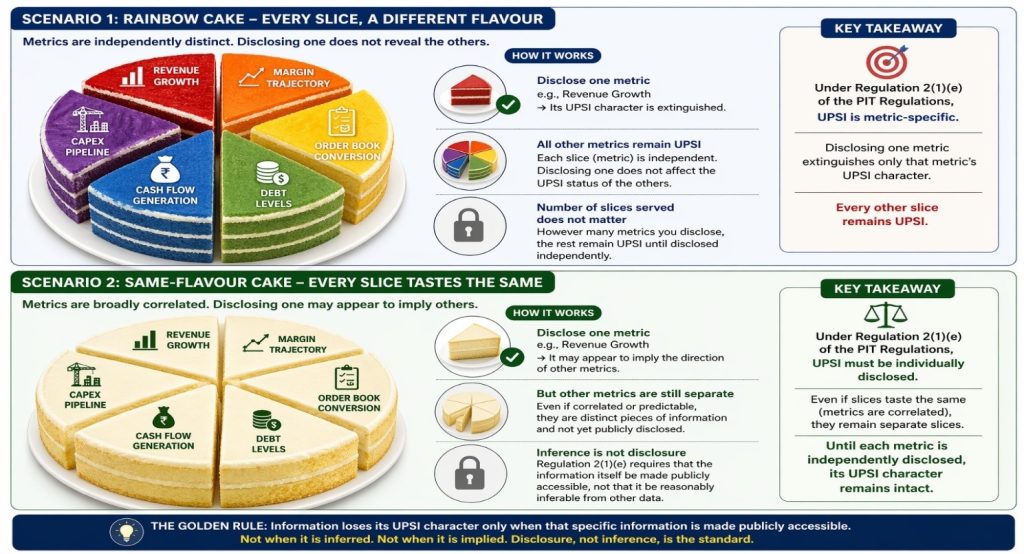

A useful way to appreciate this is through the analogy of a cake composed of multiple slices. The quarterly financial position of a listed company is that cake, and each slice represents a distinct category of information: revenue, margins, order book, collections, debt levels, and so forth. When a company files a voluntary business update, it serves some slices to the public while the rest remain in the kitchen, held exclusively by insiders. The UPSI character of what is served may get extinguished at the moment of filing; the UPSI character of what remains in the kitchen may remain wholly unaffected. This principle holds across two scenarios that are worth distinguishing.

The first is a rainbow cake, where every slice carries a completely different flavour, a company whose metrics are independently distinct, where revenue growth tells the market one thing, margin trajectory another, order book conversion a third, and debt levels a fourth. Here, the position is straightforward: disclosing one metric extinguishes the UPSI character of that metric alone, and every other slice remains UPSI regardless of how many slices have been served.

The second scenario involves a cake where every slice carries the same flavour, a company whose metrics are broadly correlated, such that disclosing revenue might appear to imply the direction of volumes, realisations, and margins as well. A company in this position might reason that disclosing one metric has effectively communicated all the correlated ones. That reasoning does not hold in all circumstances. The standard under Regulation 2(1)(e) of the PIT Regulations requires that information itself be made publicly accessible, not that it be reasonably inferable from other disclosed data. Until each metric is disclosed independently, its UPSI character remains intact, regardless of how predictable it may appear given what has already been shared.

The interaction between the likelihood test and the extinguishment principle thus creates a two-stage framework. At the pre-disclosure stage, management holds UPSI. At the post-disclosure stage, the UPSI is extinguished only if the filing is complete, simultaneous, and non-selective. It must, however, be emphasised that whether UPSI has been extinguished in any given case is not a conclusion that can be reached in the abstract. The determination requires a careful, fact-specific examination. Each case must be assessed on its own facts and circumstances before concluding whether UPSI is extinguished, and most importantly, which facet of it.

Furthermore, the company’s trading window policy must be observed. The trading window for insiders remains closed until 48 hours after the publication of financial results under Regulation 33 of the LODR Regulations, pursuant to the PIT Regulations (Schedule B, Para 4(2) read with Para 5), regardless of whether a voluntary operational update has been filed. A voluntary quarterly business update does not substitute for the formal results filing for trading window re-opening.

V. International Practice: A Comparative Snapshot

The practice of voluntary quarterly updates is well-established internationally, though the regulatory architecture surrounding it varies considerably across jurisdictions.

In the United States, Regulation Fair Disclosure (“Reg FD”), promulgated by the SEC in 2000, was a watershed: it prohibits selective disclosure of material non-public information to analysts or institutional investors without simultaneous public disclosure. Reg FD requires that such information be disseminated broadly to the market, and while filing a Form 8-K is an expressly permitted method of compliance, it is not the only one. In practice, however, many S&P 500 companies use Form 8-K to disclose material information shared in investor presentations or earnings calls. Companies also frequently provide “pre-announcement” updates, guidance revisions, and preliminary results through such filings. The safe harbour for forward-looking statements under the PSLRA provides meaningful protection for these disclosures when appropriately caveated.

In the United Kingdom, the current disclosure framework is governed by the UK version of the Market Abuse Regulation, particularly Article 17, as reflected in the Financial Conduct Authority’s Disclosure Guidance and Transparency Rules, including DTR 2.2.1A and DTR 2.5.1A. Issuers are required to disclose inside information to the public as soon as possible, except in limited circumstances permitting a delay where immediate disclosure would prejudice legitimate interests. The UK eliminated mandatory quarterly reporting for listed companies in 2014, following the EU’s repeal of the Transparency Directive’s quarterly reporting requirement, precisely to reduce the short-termism associated with mandatory quarterly disclosures. Voluntary updates continue, but are company-driven.

In the European Union, the Market Abuse Regulation (Regulation 596/2014), particularly Article 17, requires issuers to disclose inside information as soon as possible publicly and expressly prohibits selective disclosure. The regime allows for delayed disclosure under specified conditions but maintains a strong emphasis on continuous, price-sensitive disclosure. As with India’s Regulation 30 of the LODR Regulations, MAR imposes an obligation to disclose material information that may affect prices, and voluntary updates that contain inside information fall within this framework.

The consistent international theme is that voluntary disclosures are permissible and encouraged, provided they are simultaneous, non-selective, properly filed through regulated channels, and do not substitute for mandatory periodic disclosures.

VI. Best Practice Framework for Indian Listed Companies

Drawing from the regulatory framework and international practice, listed companies that choose to file voluntary quarterly business updates should adhere to the following principles:

- Disclose through exchanges and all relevant means: All voluntary disclosures must be filed on stock exchanges to satisfy the “generally available” standard under the PIT Regulations. The exchange filing is a necessary condition, but not the only channel through which broad-based, non-discriminatory dissemination must be achieved.

- Disclose completely, not selectively: Consistent with the principles of truthfulness, accuracy, and completeness mandated by Regulation 4(2) of the LODR Regulations, if a company discloses revenue, it should also disclose any material headwinds on margins. A disclosure designed to present only a positive picture, in the manner of cherry-picking, may constitute a fraudulent trade practice under the PFUTP Regulations and will not extinguish the UPSI character of the withheld adverse information.

- Maintain trading window discipline: A voluntary update does not reopen the trading window. Compliance officers must track the 48-hour window post-formal results.

- Include appropriate cautionary language: Forward-looking statements should be clearly labelled as estimates and accompanied by risk factors and assumptions, to the extent possible under Indian law.

- Board / Audit Committee sign-off: While not legally mandated, best practice requires that voluntary updates be reviewed and approved by the Chief Financial Officer and Company Secretary, and ideally noted by the Audit Committee, before filing.

- Consistency: A company that begins issuing quarterly updates creates a reasonable market expectation of continuity. Abrupt discontinuation of updates, particularly in a weak quarter, may itself be interpreted by the market as a signal and could attract scrutiny.

VII. Conclusion

Voluntary quarterly business updates are, at their best, a genuine act of transparency, one that reduces information asymmetry, narrows the gap between market expectation and reality, and signals governance confidence. The regulatory framework neither prohibits them nor mandates them. That discretion, however, is not without consequences, and this article has attempted to show that the answer lies in a clearer understanding of what voluntary disclosure actually commits a company to.

The analysis reveals a paradox that sits at the heart of selective voluntary disclosure. Consider three positions a company can occupy. The first is a company that discloses nothing voluntarily and waits for formal results: insiders hold UPSI, the trading window is closed, and the framework operates exactly as designed. The second is a company that discloses everything completely, simultaneously, and without cherry-picking as part of voluntary disclosures: UPSI is extinguished, the market is fully informed, and the principles of Regulation 4(2) are honoured. The third is a company that does something in between, disclosing the metrics that look good and withholding the ones that do not. That third company, despite its apparent effort at transparency, is in the most legally exposed position of the three. It has partially re-priced the market, it continues to hold undisclosed UPSI, and it has achieved this uncomfortable position entirely by its own choice.

The market data discussed in this article makes this more than a theoretical concern. The price movements observed across the companies studied confirm that voluntary operational and financial disclosures made prior to the publication of quarterly financial results under Regulation 33 may be price-sensitive. Such voluntary disclosures do not, by themselves, create the regulatory risk. They either put that risk to rest or deepen it, depending entirely on the quality, timing and completeness of the disclosure.

The framework, as it stands, is already sufficient. Regulation 4(2) of the LODR Regulations, the three-limb UPSI test, the granular extinguishment principle, and the trading window rules together provide everything a company needs to navigate this practice responsibly. What is required is the recognition that a voluntary quarterly update is not a communication exercise or a market management tool; it is a legal act with specific, fact-dependent consequences that are not easily undone once the filing is made. The company that approaches voluntary disclosure with the same rigour as any other exchange filing, disclosing completely, consistently, and without omission, is the one for whom this practice fulfils its promise. The company that does not, walks straight into a trap entirely of its own creation.